Options/NET · .NET Library

Multi-leg strategy analysis, built for .NET

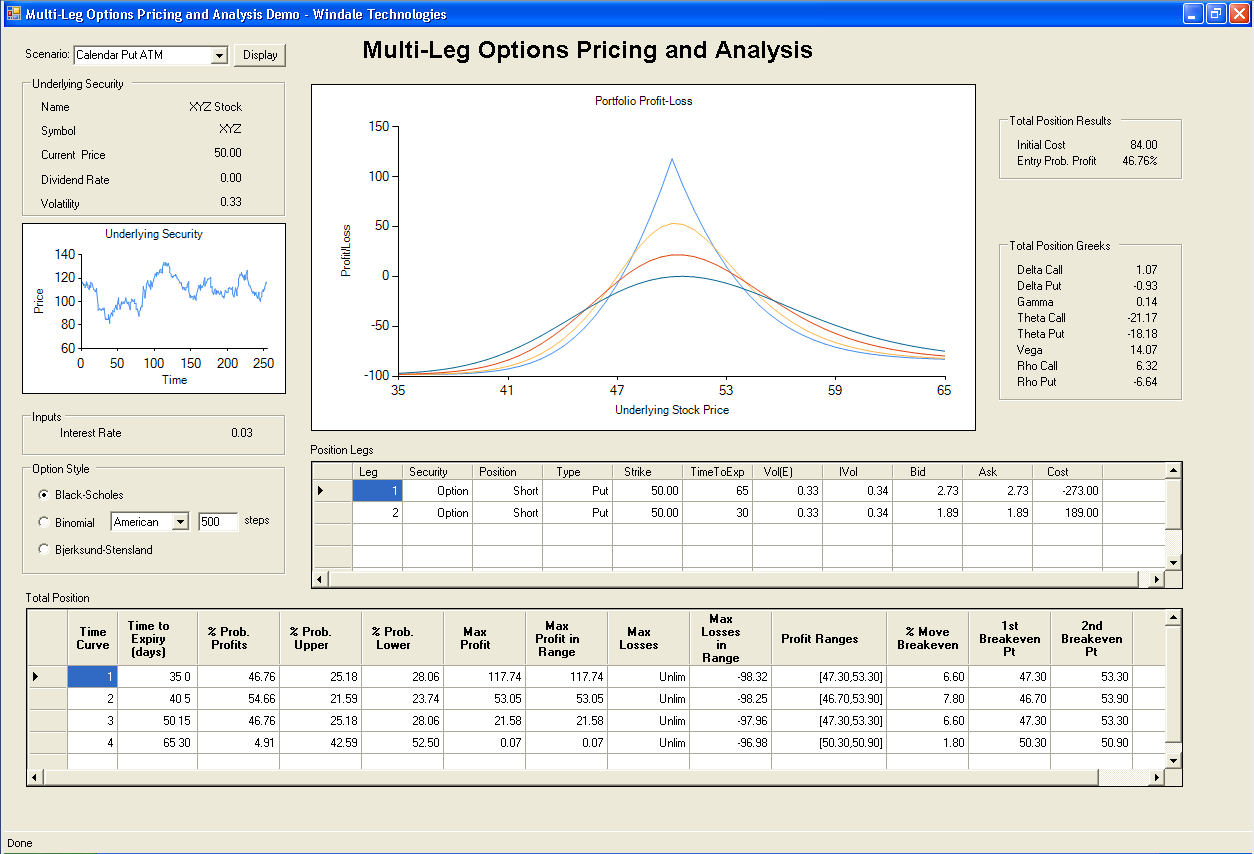

Options/NET is a comprehensive .NET component for analysing complex options strategies. Build proprietary analytics for Iron Condors, Butterflies, Calendar Spreads, Straddles, Strangles, Ratio Writes, and more — with full profit-loss charting and scenario analysis built in.

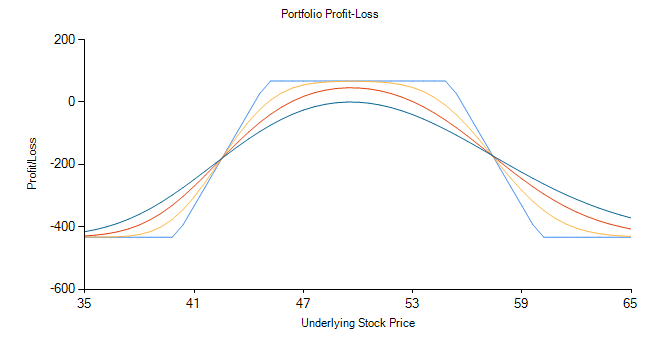

Iron Condor — Profit-Loss Chart